Jubilee

Metals Group plc: Get ready for Lift-Off.

Counting down from six months to the end of H2 2024 (June 2024) for Jubilee

Metals Group (“JMG”). 6, 5, 4, 3, 2, 1 months and we will have lift-off. With

January and February 2024 already in the past, only 4 counts remain.

The new Jubilee Metals Group was born just over ten years ago when it

transitioned to essentially an innovative specialist metallurgical business

model. It targeted a huge greenfield gap in the smelting and beneficiation of

above ground mineral “ore” stocks in waste or discard materials. Most of these

materials were left-behind pollutants of legacy mines, materials considered

uneconomical to process.

"All overnight success

takes about 10 years."

Jeff Bezos At The

Economic Club Of Washington (9/13/18)

JMG developed the technologies to change that and turn rubbish to gold so to

speak, literally turning waste materials into valuable commodities. Alchemy at

its best. Over ten years in the making, now JMG is ready for that overnight

success. I am expecting it to happen in H2 2024.

JMG proved its technologies and its expertise in the processing of chrome

with Platinum Group Metals (“PGM”) as a byproduct. The essence of innovation is

not in the product but in the technology and a “good” technology will migrate

across similar products. JMG excelled in its chrome processing and then once

again identified a unique greenfield opportunity in Zambian copper waste and

discarded materials.

The ten-year path to overnight success started with the identification of a

unique metallurgical opportunity. The next phase was the strategic move into

copper. Chrome and PGM is now a reliable mature business. Copper is the new

horizon for JMG, and it’s moment has arrived.

Copper

The defining copper strategy event was the acquisition of the Sable Refinery

in August 2019 almost 5 years ago. Halfway towards its 10-year overnight

success. The rundown Sable refinery was repurposed and innovatively modernized.

It was also converted to a modular expansion plant, designed on the foundations

of the innovative technologies developed for the chrome business. The Sable

Refinery has since been supplemented with the, also modular, Roan

Concentrator. A unique and innovative processing plant purposely designed to

accept a wide range of copper bearing materials for processing to refinable

copper concentrates at a single facility. Feedstock from Roan is refined to

copper cathode at Sable as part of the strategy to reach 25,000 tonnes of

copper production made up of a combination (around 50/50) of copper concentrate

and copper cathode (Interim

Results Presentation, Slide 6, CFO comment).

The transition of innovative technologies was proven with copper. A

different commodity, a different country, but the true value locked away from

sight is the technological competence of JMG. Copper production was initiated,

the technologies tested and reshaped for copper. It is still being perfected

yet production of copper at around 1,500 tonnes in FY 2021 is targeted to reach

almost 6,000 tonnes in FY 2024. Reported progress is that copper production

capacity is expected to reach 25,000 tonnes already in FY 2025. Copper

production at those levels will not be far behind given the track record of

JMG.

Copper production for FY 2023 was just short of 3,000 tonnes. Doubling to

almost 6,000 tonnes in FY 2024 is guided (confirmed in the recent Interim

Results Presentation). Copper production, even at the lower pre-2024 levels, is

exceptionally profitable with gross profit margins around 40%! Copper

production at full capacity of 25,000 will be transformative for JMG and yet it

will still only be the completion of the first step in its copper journey.

Low-cost mineral production from discards is at the heart of JMG’s technology.

Combine that with production economies of scale for break-out company

profitability and that instant success ten years in the making is right here

starting in H2 2024. FY 2025 will be the defining annual “moment”, be ready for

it.

The next phase in the copper journey will be the implementation and

integration of the recently announced new copper initiatives in Zambia.

JMG announced a new Slag

Project with Mopani Copper Mines in October 2023 (now named the

Mufulira Slag Project). Mopani Copper Mines has since been acquired by Abu

Dhabi based International Resources Holding RSC Limited ("IRH"). The

Mufulira Slag project targets profitable processing of 13 million of historical

slag containing an estimated 0.7% copper and 0.27% cobalt as a testament to its

expertise and technological competence. The Mufulira Slag Project is estimated

to yield 89kt of copper and 44kt of cobalt. The context is that this single

project would supply the equivalent of more than 3 years of copper full

production at 25,000 tonnes pa as a still to be unlocked growth initiative.

JMG and IRH entered into an additional new JV development arrangement, the Waste

Rock Project. The fundamental deal is that JMG will provide the

technological processing expertise for the JV and IRH will provide the funding

and financial support, certainly a match made in business heaven. JMG surveyed

the available materials for processing to be 260 million tonnes on surface. No

digging or blasting for it. The materials are suitable for both concentrate

production and for refining copper cathode in this yet another unfolding growth

initiative.

The

Munkoyo Project ("Munkoyo") is located within 50

kilometers of Sable and will be another feedstock source for Sable. JMG has

tested and refined about 80,000 tonnes of mined ore from Munkoyo at copper

grades ranging from 1.5% to 3%. Munkoyo has significant near surface copper

ores and further exploration will illuminate the total extent of this

opportunity as a longer-term additional feedstock sustainability project. JMG

has an option to acquire the Munkoyo Project. The higher grades of the Munkoyo

project are like copper candy for JMG.

The mature chrome business is not static and is targeting production growth

to exceed the production of 2million

tonnes of chrome concentrate. That capacity target is expected to be

achieved by FY 2025. The main driver behind the chrome growth strategy is owned

production with the expansion of the Thutse

Project adding a further 50 000 tonnes per month feed

processing. That in turn allowed for the implementation of an additional

300,000 tonnes pa chrome concentrate production module targeted for Q3 2024

(reporting period FY June 2024 so Q3 is Jan -March 2024). The new module would

bring chrome concentrate production capacity to 1,75mil tonnes pa before FY

2024. More advances from Thutse can be expected.

JMG Interim Results 2024 (six-month period

ending December 2023)

The H1 Interim

Results have recently been released.

- "Group revenue increased by 18.4% to £74.7

million (H1 FY2023: £63.1 million) driven by increased production during

the period.

- Group earnings before interest, tax,

depreciation and amortisation (EBITDA) increased by 13.6% to £11.7 million

(H1 FY2023: £10.3 million).

- Group profit after tax increased by 7.3%

to £4.4 million (H1 FY2023: £4.1 million)

- Earnings per share increased by 6.7% to

0.16 pence per share (H1 FY2023: 0.15 pence per share)"

Full year production guidance for copper remains at 5,850 tonnes, similarly

PGM production guidance is held at 42,000 oz. Chrome production is expected to

exceed the 1.45 million tonnes guidance as was discussed above with the

addition of a further chrome production module in Q3 2024.

These results were achieved despite the PGM disastrous price collapse. The

PGM GBP revenue dropped by 26.8% from lower production, lower prices, and

higher costs. The PGM gross profit margin collapsed by 81.6% and yet the JMG

posted interim results were impressive with an 18.4% increase in Group Revenue,

13.6% increase in EBITDA and earnings per share growing by 6.7%. The main

driver behind the sterling results, almost fully mitigating the PGM disaster,

came from the chrome growth strategy, higher chrome prices, the Thutse chrome

owned production drive and the move from fixed external processing margins to

price variable gross profit margins. The chrome business result is that the

gross profit margin on higher chrome production increased by 240%.

The growth in copper production, combined with the excellent chrome results,

is expected to more than fully mitigate the PGM business unit decline.

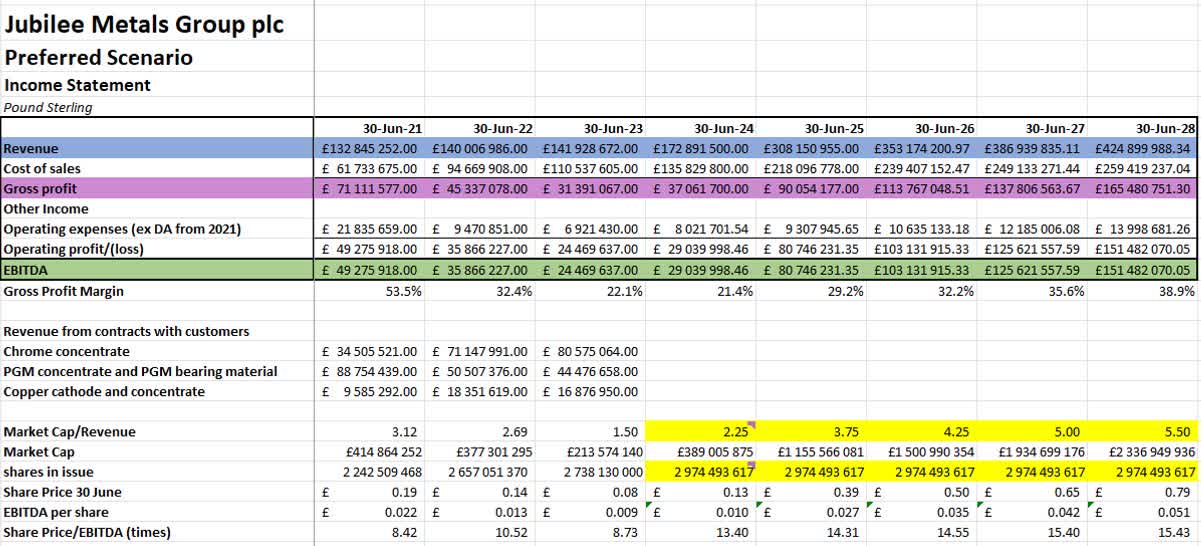

Updating the JMG Scenario Model

The income statement model comes in two parts. The foundation is the

division into business units, chrome, PGM and copper. The details are then

consolidated into a JMG income statement.

The business units data have been updated from the information supplied by

the company in its Interim Financial Report for H1 2024 as well as from details

supplied in the Interim Results Investor Presentation (both already linked

above).

Source: Data from JMG, model built by Sarel Oberholster (click on the image for a larger view)

The most important developments have been:

- The solid growth in chrome production supported by a robust

chrome price increase achieved.

- The implementation of another 300,000 tonnes pa chrome

production capacity module with expected chrome production capacity

reaching 2million tonnes by FY 2025 (June 2025).

- The accelerated expansion in copper production with an

expectation that copper production capacity will breach 25,000 tonnes in

FY 2025.

The severity of the PGM decline is probably unsustainable as the industry

simply cannot maintain market supply at these depressed price levels. I expect

the PGM prices to rather advance from here which could add to better results

for JMG, but JMG results are about to pop even if the PGM prices remain at

these levels.

The production advances in chrome, but by far the most important, the

production advances in copper will catapult JMG revenue to a new level. I have

highlighted in dark blue the FY 2025 expected production advances. The

viability of the copper strategy comes into sharp focus when we look at the

copper revenue jumping from around £17mil in FY 2023 to around £31.5 expected

in FY 2024, then moonshot to an expected £132mil in FY 2025 on the back of

production growth. The chrome growth strategy is not as spectacular but still

incredible with chrome revenue advancing from £80.6mil in FY 2023 to an

expected £109mil in FY 2024 to reach an expected £142mil in FY 2025.

The effect on JMG consolidated results is equally moonshot spectacular.

Source: Data from JMG, model built by Sarel Oberholster (click on the image for a larger view)

Group revenue is expected to top £308mil by FY 2025 from a reported £142mil

FY 2023 with the jump to £173mil for FY2024 almost as “nice”. FY 2024 is the

potatoes; the meat arrives in FY 2025 with EBITDA jumping from less than £25mil

in FY 2023 to almost £81mil expected in FY 2025.

Investors in JMG will have their full plate of meat and potatoes by FY 2025.

Its all under the radar presently. The share price remains mired in the

doldrums. JMG gives the information to the market, yet it seems nobody

believes. Then the market wakes up on one unpredictable trading day and over a

few trading days advance the share price by 200% or 300%. The share price

target for FY 2025 for JMG is 39 pence from the current share price drifting

around 5 pence. I’ve seen this slumber and explode share price moves happen

often enough. Will you be there when it happens, or will you try and catch the

rocket as it makes its moonshot, or will you remain unconvinced and tell the

story of how you almost caught that big one? As disclosed, I have a ticket.

Sarel Oberholster

4 March 2024

![[Most Recent Quotes from www.kitco.com]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_sR-oM5h8MrvOlcQfuCjujI8-b4scVCg_IA0rRVWLRIPChH5XYL9JCk4wIzchePwRRGUU5Xq-uyZUnEahSNMtSy0zPi0DbR6QeVGSjcmVxdNjdu_PS0LEnk4twEdQ4OwYwmqQ=s0-d)

![[Most Recent Charts from www.kitco.com]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vLwYCDjtcNlF-CukBcySuIaGvxf1zDn6wHuG9VyoFqsGo8uXrTQyWVzOFTz7FEOduHizkfSoud75VYOCtsVAMJCDaCIgvq6dwUXCHBzkVMX5dO8ECap8HZkU1QsnC_TTyz4RfsisQ=s0-d)

![[Most Recent Quotes from www.kitco.com]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vbieldYyF_oXErzyQ6vAK7WRuiVAsbrs8a8ZGtA35XT2u3VZOV5VfJlfHDu-Nh1oEf3-cejnpkiaQ4xIsh7Rwxv32JqLLkgGHopUpN2_u1BG4_87F6WbwhHDmtT20bGw=s0-d)

{kind=link}

2 comments:

The electronics delay for the Roan upgrade has now impacted the copper production with guidance revised down to 3250-4000 tonnes from 5850. They were probably overoptimistic at Interims stage and should have downgraded then. Chrome, however is trending and will probably more than compensate for the copper delay. I will treat the dip as an entry point rather than reason to sell.

https://tools.eurolandir.com/tools/Pressreleases/GetPressRelease/?ID=4503174&lang=en-GB&companycode=uk-jlp&v=

Roll-out of Integrated Copper Strategy in Zambia

Acquisition of two near-surface copper mining operations

https://tools.eurolandir.com/tools/Pressreleases/GetPressRelease/?ID=5179971&lang=en-GB&companycode=uk-jlp&v=v2024

Highlights

Roan Operation

§ Jubilee concludes a further off-take agreement for stockpiled low grade mined material (LG Material) in support of the expanded Roan operations (Roan Operations).

o The LG Material is upgraded at source prior to further processing at Roan.

o The upgrading of this LG material has commenced in preparation for the ramp-up at Roan.

§ The Roan Upgrade has completed construction with operational readiness testing commencing. The electrical control system (ECS), originally delayed, is undergoing testing before final implementation expected during July 2024.

§ The Jubilee team has commenced with pre-processing of targeted feed material destined for Roan in preparation of an accelerated commissioning and ramp-up during July 2024.

Copper Resource Transactions

§ Jubilee concludes two copper resource transactions of operating open-pit mines accessing near-surface copper material (open-pit operations) which significantly increases its copper resource base (Acquisitions).

My view remains to accumulate.

Post a Comment